Search Data Predicts Massive Market Shifts in the Weight Loss Industry

May 30, 2025|Read time: 6 min.

A tsunami is sweeping through the weight loss industry impacting consumer behavior and upending market dominance.

Since the 1960s diet brands like Weight Watchers, Slim Fast, and Jenny Craig have dominated the weight loss industry. But 2021 was an inflection point ignited by the booming popularity of weight loss injections.

Now, massive pharmaceutical brands like Eli Lilly and Novo Nordisk are becoming the global leaders, and the competition is just starting to heat up.

With consumer interest surging and 16 new drugs entering the market by 2029, it’s no wonder analysts estimate the market for obesity treatments could reach $200 billion by 2031.

As the weight loss market undergoes a sea change from health foods to healthcare, pharma companies will find themselves competing against a much wider range of brands in a digital arena where they don’t yet have the high ground.

Until recently, pharma brands have focused on brand marketing through broadcast and streaming services. Few companies have experience engaging with consumers directly by publishing long-form web content.

But as awareness grows for weight loss medication, more consumers will turn to search engines for answers. If pharma brands don’t evolve their marketing strategies to meet them where they are, they’ll risk losing market share as the industry explodes with opportunity.

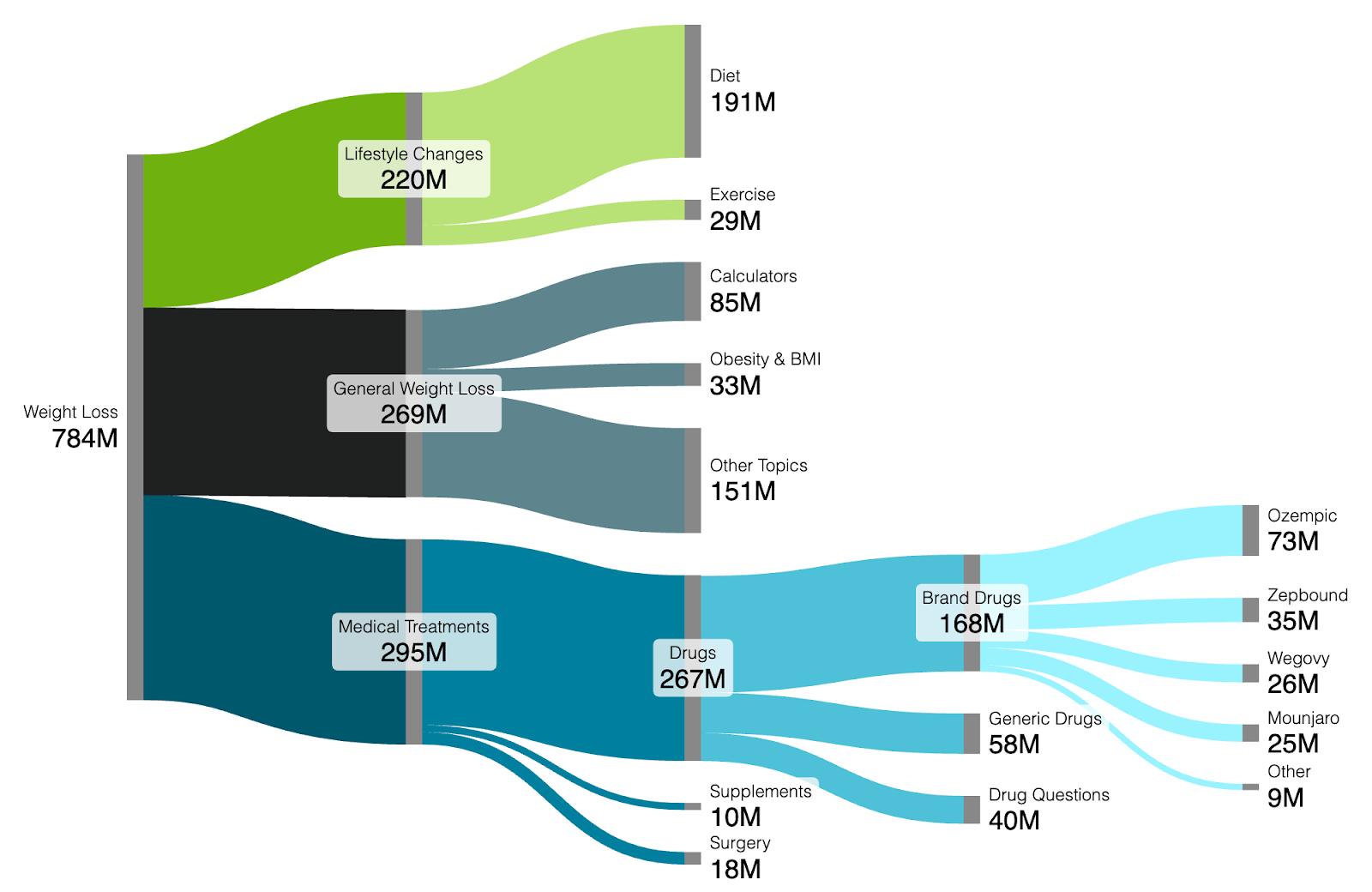

Mapping 784 million weight loss searches

Using Terakeet’s patented Total Addressable Market (TAM) technology, we uncovered 784 million annual searches about weight loss and segmented them into three groups:

- General weight loss

- Lifestyle changes

- Medical treatments

In the general weight loss segment, searchers want to understand obesity, learn about different weight-loss options, or use calculators to help them stay on track, set goals, and measure progress.

Consumers in the lifestyle changes segment have decided to take action, and they want to change their behavior to lose weight. Consumers in this category overwhelmingly search for diet options over exercise to lose weight.

[NOTE] The total addressable market for all exercise topics is much bigger than the weight loss exercise segment we included here. That’s because it is important to consider intent. People exercise for many different reasons beyond weight loss, including strength training and general fitness. So we focused on exercise topics related to weight loss specifically.

The medical treatments segment is dominated by medication searches. In this group, consumers want general information about “weight loss medication” and “appetite suppressants” as well as specific details about the cost, side effects, and dosing of both brand name and generic drugs.

Brand-name drugs have strong awareness in the weight loss industry. Nearly 22% of all weight loss searches we analyzed mention a brand-name drug.

Among them, Ozempic has the highest search demand.

[NOTE: We included drugs like Ozempic and Mounjaro even though they aren’t approved for weight loss because consumers search them when seeking weight loss medication]

Grouping the search data by manufacturer, we learn that Eli Lilly and Novo Nordisk control 97% of the brand name drug searches for weight loss, and that Novo Nordisk has a comfortable lead in terms of brand awareness.

Source: Terakeet

Pharma brands lack visibility for weight loss drugs

To find out which brands influence purchasing decisions for weight loss drugs earlier in the buying journey, we filtered out brand name drugs from our data and focused on searches for generic drugs and general weight loss drug questions.

This segment includes searches like “semaglutide,” “tirzepatide,” and “orlistat,” as well as “weight loss injections,” “appetite suppressant,” and “best weight loss pills.” These types of searches often occur early in the consumer decision-making process, before a specific brand is chosen.

It’s important for brands to be visible for these types of searches because they drive awareness, affinity, and consumer choice. This is one of the most critical segments for pharmaceutical companies to control because it influences product sales. Being present in these moments helps brands shape the conversation, highlight differentiators, and educate potential customers before they’ve committed to a particular product.

However, we found that pharmaceutical brands only controlled 6.9% of organic search market share in this segment while healthcare providers and medical publishers earn more than two-thirds of consumer attention.

Source: Terakeet

Mayo Clinic is the segment leader with 18% search market share. As an incredibly trusted medical brand, it deserves its top-ranking position. But its success is based on more than its reputation.

Mayo Clinic published more than 100,000 pages on its website about diseases, conditions, disorders, symptoms, procedures, treatments, drugs, and more. The library of content includes thousands of expertly written pages dedicated to weight management, including calculators, weight loss tips, and medication advice. Each page is reviewed by specialty medical editors.

On the other hand, pharmaceutical brands like Eli Lilly and Novo Nordisk are falling short of their potential. They are experts in the space, having created the treatments being discussed by third-party websites.

Source: Terakeet

As the weight loss industry shifts further towards medical treatments, pharma brands will need to adapt their market strategies to publish more informational content for consumers.

Pharma brands are invisible for general weight loss topics

The general weight loss segment has plenty of opportunities to connect with consumers, offer value, and guide decisions at the beginning of the journey. Yet pharma brands had zero visibility in this category.

Low-hanging fruit includes 84 million annual searches for calculators, charts, and tools related to weight loss. These searches are currently owned by generic calculator websites that control 15% of search market share in this category.

Pharma brands could create their own tools with a much better experience to meet the needs of consumers struggling with weight loss.

Source: Terakeet

Trend data reveals an inflection point for weight loss treatments

Consumer search interest in weight loss medication has surged over the past five years, growing at a compound annual growth rate (CAGR) of 48.18%, and reaching a record high in May 2025.

For the first time, more people are seeking drugs over diets as the solution to weight loss. Established brands like Weight Watchers (WW) have lost relevance as new drugs enter the market.

Source: Terakeet

And it’s not just one keyword. There are 64 million more annual searches across the entire weight loss medication segment than the weight loss diet segment.

Source: Terakeet

Eli Lilly is poised to be the new market leader

David Moore, EVP of U.S. Operations and Global Business Development at Novo Nordisk, said the total market for anti-obesity medicines grew in the U.S. last year by 160%, and that Novo has just over half of the U.S. market share as measured by total monthly prescriptions.

However, search demand for weight loss drugs is shifting rapidly. Search interest in the U.S. for Eli Lily’s Zepbound passed Wegovy at the end of 2024 and continues to surge, indicating that it could be the new market leader in 2025.

In fact, analysts are already predicting that Zepbound will become the new market leader.

Source: Terakeet

Looking at the global market, search demand for Mounjaro is positioned to overtake Ozempic, and Zepbound is growing at a faster rate than Wegovy.

Source: Terakeet

That level of momentum is hard to reverse. Based on the trend lines, Lilly’s drugs could have more search interest than Novo’s in the U.S. and globally by the end of 2025.

Whether that translates to actual sales and market share is harder to estimate. But if more consumers are seeking out your brand than your competitors, that usually means revenue is close behind.

How do pharma brands capture unprecedented demand?

To connect with consumers in the booming weight loss industry, pharma brands will need to market like publishers. The biggest opportunities lie in the general weight loss and weight loss medication segments — specifically drug questions and generic drugs.

These categories include more than 40 thousand keywords representing 368 million annual searches.

By decoding these insights, brands can reach consumers when they’re most receptive, meeting their needs in real time and delivering exceptional experiences. Most importantly, pharmaceutical companies can ensure potential customers discover accurate and favorable brand messaging wherever and however they search.

Learn how consumer insights can drive consumer connection

What We DoUnlock instant access to 25+ digital marketing resources and the OAO 101 introductory email course to kick start your strategy.